BY RUSSELL HAGUE ⋅ JUNE 12 2015

It’s been said that if you master double-entry bookkeeping, 95% of accounting is a piece of cake. I’m not sure about that but there are various hints and tips that can help us along the way. PEARLS (purchases, expenses, assets on debit side then revenue, liabilities, sales on the credit side) and DEAD CLIC (debits, expenses, assets, drawings on one side and credits, capital, liabilities, income, on the other side) are a few which springs to mind but here’s another, one which may be helpful if you haven’t covered every base with any of the other methods.

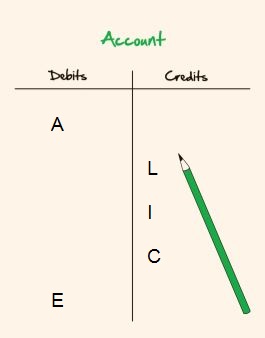

Meet ALICE!

There are only 5 different categories to remember with this method in which the first letter of each spells ALICE when arranged in that order.

The first thing is to decide what ‘type’ of transaction you are working with, does it represent an:

Asset,

Liability,

Income,

Capital, or

Expense?

Secondly, you need to ascertain which side of the account an increase or decrease in value relates to. This sounds harder than it actually is.

Increase in:

Asset > Debit

Liability > Credit

Income > Credit

Capital > Credit

Expense > Debit

A decrease in any of the accounts is just the opposite.

Decease in:

Credit < Asset

Debit < Liability

Debit < Income

Debit < Capital

Credit < Expense

If you can commit that to memory, you’re helping to set yourself up for your future AAT studies and career in accounting.

One tactic is just to remember an ‘increase in assets or expense is a debit’. That’s it. At the start of your task, write on your scrap paper ALICE and debit next to the A and E. It follows that the others must be credits.

So, when presented with money received into the bank and asked which double-entry to make, consider that the bank is an asset, therefore an increase must be a debit. The other part of the double-entry, (e.g. sales income), must be the opposite – a credit.

When posed with the task of recording a payment from the bank account, to purchase stock for example, the amount of the asset which is money in the bank decreases, you’ve paid money out of it; therefore the entry in the bank account must be a credit.

It follows that the opposite account entry must be a debit – in this case to the purchases account. (You are actually increasing an asset by increasing the existing stock by the value of what you’ve just bought. In effect swapping one asset, cash, for another asset of equivalent value, stock).

Let’s try one more example, this time using transactions recording credit sales to customers in one of the books of prime entry you will be working with, the sales day book.

Sales day book

Date Details Folio Gross VAT Net

1.2.XX. M Hatter SL 120.00 20.00 100.00

5.2.XX. W Rabbit SL 240.00 40.00 200.00

Totals 360.00 60.00 300.00

Let’s decide which general ledger accounts we are using here and which classes of accounts we are dealing with?

Gross total sales are recorded in the sales ledger control account.

This is an ASSET – money owed to the business which is expected to be paid and we’re increasing it, ask ALICE? It’s a DEBIT entry.

DR General Ledger – Sales Ledger Control Account CR

Date

Details

£

Date

Details

£

28.2.XX. SDB 360.00

VAT total is recorded in the VAT account. Its money we’ve collected on behalf of the HMRC and we will have an obligation to pay it on to them. Since we owe it to them, this is considered a LIABILITY. We’re increasing the liability so ask ALICE? It’s a CREDIT entry in the VAT account.

DR General Ledger – VAT Account CR

Date

Details

£

Date

Details

£

28.2.XX. SDB 60.00

Net total – this is SALES INCOME which we’re increasing therefore, according to ALICE, it’s a CREDIT entry in the sales account.

DR General Ledger – Sales Account CR

Date

Details

£

Date

Details

£

28.2.XX. SDB 300.00

What about the customers’ individual accounts in the sales ledger? We need to record entries here to keep track of our debtors.

It must be taken into account that each individual customer’s account is held in the sales ledger which is a subsidiary ledger outside of the general ledger accounts which we’ve looked at above.

The sales ledger holds customers, customers are debtors, debtors are ASSETS. We are increasing the debt, so increasing the asset, and therefore, according to ALICE, it’s a DEBIT entry in the customer’s account.

DR Sales Ledger – M Hatter CR

Date

Details

£

Date

Details

£

1.2.XX. SDB 120.00

DR Sales Ledger – W Rabbit CR

Date

Details

£

Date

Details

£

5.2.XX. SDB 240.00

Another name for a control account is a ‘totals’ account. It makes sense that the sales ledger control account reflects the total of all the different customers’ accounts in the subsidiary sales ledger.

This way, all the individual customers’ accounts are represented by a single entry in the general ledger – the ‘sales ledger control account’. This single amount reflects the total debtors, receivables or trade receivables.

If we didn’t use a control account you could end up with hundreds or even thousands of individual customer accounts clogging up the general ledger.

Note: in the example above, the two totals add up to £360.00 – which is the same as the sales ledger control account balance in the general ledger and provides an opportunity to reconcile our transactions.

ALICE may be able to help AAT students to unlock the curious mysteries of double-entry bookkeeping, she can’t tell you everything but she deserves some credit!